New energy storage: installed capacity exceeds pumped storage for the first time, with a target output value of over 3 trillion yuan by 2025

The latest statistical data from the Zhongguancun Energy Storage Industry Technology Alliance (CNESA) shows that in 2024, the installed capacity of new energy storage in China exceeded pumped storage for the first time.

On January 15th, the Energy Storage International Summit and Exhibition 2025 Press Conference and CNESADataLink 2024 Energy Storage Data Release Event were held in Beijing. At the meeting, Chen Haisheng, president of Zhongguancun Energy Storage Industry Technology Alliance (hereinafter referred to as “CNESA”) and director/researcher of Institute of Engineering Thermophysics, Chinese Academy of Sciences, comprehensively summarized the development of new energy storage industry in 2024 and looked forward to the development trend in 2025.

According to incomplete statistics from the CNESADataLink global energy storage database, as of the end of 2024, China’s cumulative installed capacity of electric energy storage exceeded 100 gigawatts for the first time, reaching 137.9 GW. The installed capacity of new energy storage exceeded pumped storage for the first time, reaching 78.3 GW/184.2 GWh, with a year-on-year increase of 126.5%/147.5% in power/energy scale.

Figure 1 Cumulative installed capacity of new energy storage systems in operation in China (as of the end of December 2024)

In 2024, China’s new energy storage will add 43.7GW/109.8GWh to operation, a year-on-year increase of 103%/136%. From a regional distribution perspective, Xinjiang and Inner Mongolia rank first in terms of energy scale and power scale, and are also provinces dominated by new energy distribution and independent energy storage, respectively.

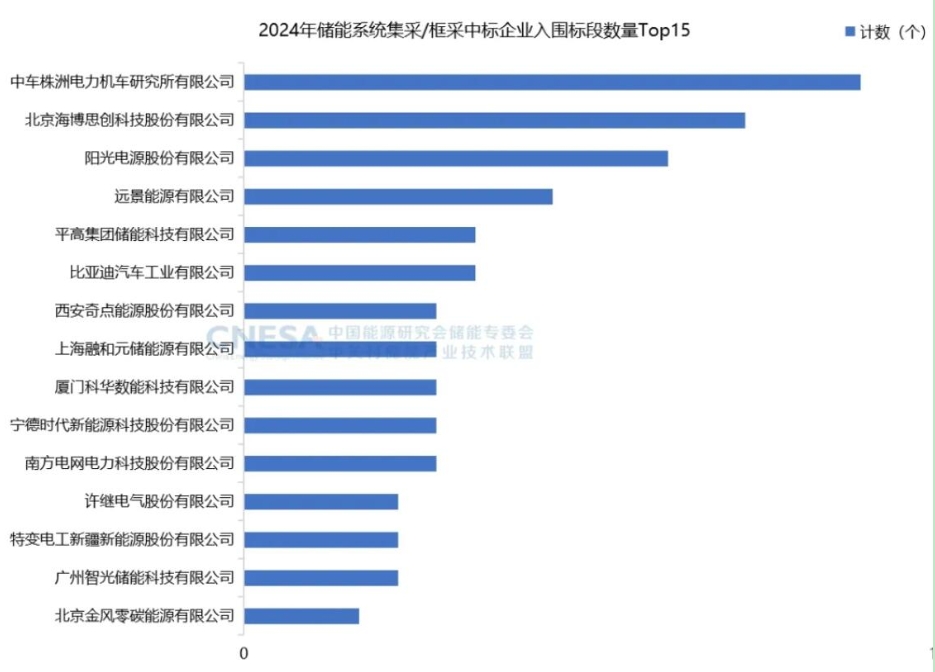

The decline in the average bid price of energy storage systems is slowing down. The scale of the new energy storage bidding market continues to grow. In 2024, a total of 528 companies released energy storage system procurement information, and 1105 companies released EPC procurement information, with year-on-year growth of 68% and 115% respectively. Due to the increasing standardization of energy storage systems, more and more large state-owned enterprises are choosing to adopt centralized procurement/frame procurement. In 2024, there were a total of 217 winning bid sections, with 46% of the total number of centralized/frame procurement bid sections among the TOP15 enterprises. From the technical requirements of centralized procurement/frame procurement, on the one hand, the qualification threshold for suppliers has been raised, and the requirements for product shipment performance, project performance, research and development strength have been further tightened. Leading enterprises have strong competitive advantages; On the other hand, it has a large scale and strong appeal to enterprises, making it the main battlefield for low-priced bidding.

Figure 2 Top 15 shortlisted bidding companies for the 2024 energy storage system centralized procurement and frame procurement

From the perspective of the entire bidding market in 2024, there are three characteristics. One reason is that EPC dominates the bidding market, and in 2024, the scale of EPC bids and the number of winning companies are higher than those of energy storage systems; Secondly, the market competitiveness of top integrated enterprises is becoming stronger, with the bidding scale of the top 15 energy storage system enterprises reaching 57% of the total bidding scale, further increasing compared to last year; The third is the procurement of individual projects, and owners are more inclined to achieve turnkey projects through EPC bidding.

In terms of winning bid prices, the decline in the average winning bid price of energy storage systems in 2024 has slowed down. The annual average winning bid price of 2-hour lithium iron phosphate energy storage systems is 628.07 yuan/kWh, a year-on-year decrease of 43%. The average bidding price of EPC has fluctuated and decreased throughout the year, with an average bidding price of 1181.28 yuan/kWh.

The target output value of new energy storage has exceeded 3 trillion yuan. From the perspective of output value planning, new energy storage, as a new engine for economic growth, has been emphasized in industrial planning in multiple regions. The output value target set by 2025 has exceeded 3 trillion yuan. In addition, several regions have proposed output value targets for 2027 and 2030, reflecting the importance that local governments attach to the planning and layout of the new energy storage industry.

From the perspective of investment and financing, there have been over 107 investment and financing events involving energy storage related enterprises in the primary market, with a disclosed amount of nearly 17.6 billion yuan, a year-on-year decrease of 70% compared to 2023. Among the financing directions, 45 are focused on system integration, charging and swapping, lithium batteries, and materials. In the field of non lithium battery technology, sodium batteries and solid-state batteries have received high attention.

What are the development trends of new energy storage in 2025?

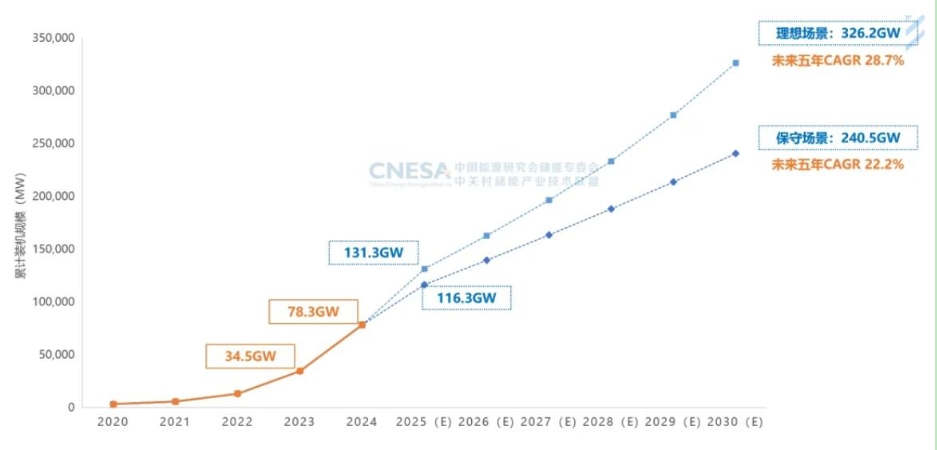

Figure 3 Prediction of cumulative installed capacity of new energy storage in China (2025-2030)

According to CNESA’s forecast, the newly installed capacity of new energy storage is expected to be between 40.8GW-51.9GW by 2025, with an average of around 45GW. At the same time, the new type of energy storage will exhibit five distinct characteristics: from the perspective of energy storage value, the value of large-scale regulation and supply guarantee will continue to increase; From the perspective of participating in the electricity market, with the continuous improvement of the market connection mechanism, the participation in market services is evolving towards the “integrated multi use, time-sharing reuse” model; The industry reshuffle is intensifying, and the number of abnormal energy storage related enterprises such as deregistration and revocation will double by 2024; Technological innovation promotes the transformation of the industry from “roll price” to “roll value”; From the perspective of market size, it is expected that the cumulative installed capacity of new energy storage will exceed 100 million kilowatts by 2025.